In recent times I’ve started to find myself more and more interested in stepping away from success. Successful teams, people, companies. I don’t mean people who are likely to be like you and me. I mean the big bosses, the billionaires, the Premier League teams… the winners.

I’m just tired. I’ve watched the world’s richest man, Elon Musk, acting like a teenager on his own social media platform. I’ve seen the super wealthy Matt Mullenweg and his eponymous Automattic, creating a fight between what he supposes is the WordPress community and WP Engine. WP Engine is the biggest of WordPress hosts out there, and worth, I dunno… a billion. Both are big big players. People in the WordPress community are not big players, by and large. Any tall poppies that come along risk being cut down by the always smiling, always affable in interviews, Mullenweg. It happened when he was OK with copying the yet to be released Drupal base theme, it happened when he pulled lots of themes by small firms from the WordPress repo, and it’s happening plenty of times since and until the WP Engine battle.

I lived in a range of places as a kid, partly because my father was a bit of an itinerant who didn’t know what he wanted in life, other than that I mustn’t live with my mother. Go figure.

Eventually I got to settle down with my grandmother, but in the process I learned a lot about life as a child in different places. Where I felt safe and where I did not.

I did not feel safe in large council estates surrounding cities. I did feel safe in a caravan park. I did not feel safe in a city centre. I did feel safe in a built up part of a large city, living in an apartment block.

At 18 I was skint and got made homeless. It took a lot of graft, patience and mistakes to get out of that and into a moderate middle class lifestyle. Here’s how.

When I was 18 I found myself in a weird situation. October 1987. I’d just started my first job, straight from 6th form, and was happy with that. My favourite song the year before had been The Future’s So Bright, I Gotta Wear Shades. I was optimistic and hopefull. I’d done my A levels finally surrounded by people who actually cared about education. I was no star pupil at 6th form, except at computers, but computers were the big thing so I had confidence.

All good then. I mean it wasn’t perfect, but I just had a fresh optimism. I’d lived with my grandmother since I was about 12 (my childhood memories are imperfect and I have few witnesses to refer to. I’d been casually fostered for a number of years prior, was fed up, and had been dumped with her. She was one of the few consistent things in my life and could see I was breaking in front of her. So I in effect ‘divorced’ my father and she took custody of me. She lived in a mobile home type caravan at the time. She was poor, but stability mattered more to me. I got my education. The future felt very bright.

I got through the various stages of ICI (then one of the largest chemical firms around) to get a job in their computer centre as a trainee printer operator, with the idea being to climb into a programming job. Unfortunately, a few weeks later, my grandmother had been in a lot of pain and, within a day of being admitted to hospital (this is another story to tell) where we discovered she had terminal cancer. Very terminal. She had less than a week left.

I was so very alone. My father turned up, signed over to me to handle everything, then disappeared to South America, never to be seen again. In 1986, my mother who I had some mild relationship with, had taken her family to Spain and, for some reason, me being told and having a goodbye seemed to be forgotten… so I’d accepted they weren’t a factor in my life. That was it. Me, alone, in the world.

Things got quite bad, quite quickly. Here’s what I learned, what I did wrong, and what I think I did right.

The world is not your friend

When you grow up, generally there are adults who look after your interests and needs, until you’re old enough to do it for yourself. But often you feel this interconnectedness with everything being generally good. Often in adulthood we discover things can be quite different – especially if we have some failures. I think learning that the world isn’t your friend is important. I discovered, for example, that if you have no cash, you can’t just take over a substantial asset (a house, in this case) and expect to not pay off debts that your grandmother had. The answer should be simple – I could have borrowed from another bank or building society to buy the house off my grandmother’s estate. Except her bank refused unless my grandmother’s estate was up to date on the mortgage payments. And because my grandmother’s estate had debts and no income, it couldn’t make the mortgage payments, and I was advised that if I paid the mortgage it would potentially make me liable for everything. When you’re an eighteen year old that leaves you in a bind.

The bank took the house, and I was made homeless, briefly (I kept a spare key and let myself in at night to sleep on the floor!), and I quickly organised myself and bought a tiny flat. Good job, because the council wouldn’t help me, the bank wouldn’t help, renting privately was almost impossible for me. Thank heavens I was organised and found the right combination of people.

Finance is risky and can be expensive

Because I was young with little credit history, all finance was risky. I figured that with my job and my flat I could now live a little and went stupid, bought myself a small engined sports car – a Scimitar SS1 1300 if you’re a car geek – a tumble dryer and washing machine all on credit, and thought everything was great. But I had nobody around to advise me I was being dumb, remember? No parents, and even most of my friends had gone off to university.

What happened was that when something went wrong with the car, it really stretched my finances to fix it. Then it got stolen and damaged, and I either repaired it myself or my insurance would get really expensive. Every little bad thing that came up, made life harder. But I discovered that I couldn’t just sell the car and forget about the finance – the interest and the way they did it meant that I’d need the value of the car plus another £1k to pay it off. I was trapped.

Toxic parents usually remain toxic parents

My father was still in touch with me, but for some reason thought I had plenty of money. So when he got into financial trouble in South America, he started giving me hard luck stories about how dangerous things were, that he was going blind (or a bit long sighted as we call it now), and he needed £1.5k. Or £3.5k in today’s money. I was 19, skint, and instead he banged on about how I must have had money from my grandmother’s death and my good job. “Yeah, Dad, but you’re not here and you have no idea.”

However, guilt led me to do my best. I sent him all my spare cash for a couple of months, before finally arranging a loan. I used some of it to consolidate my credit card debts, and two thirds went to him. I sent him, if I remember correctly, about £800 in total. He wrote to say he was struggling and needed more and he was in a dangerous situation I didn’t understand.

So I did what I felt was the right thing – I spoke to the Foreign Office, and eventually secured a facility for him to be able to catch a flight home, where he’d at least get benefits.

I called him, told him the good news, he was furious. And that was the last time I spoke to him. Ultimately, narcissistic, self-centred and selfish people rarely understand that other people have struggles. They just don’t get it. And they stay that way.

Stability matters

One thing I did right was to stay at ICI for many years. I kept that job. My head wasn’t in the best place, so I wasn’t the best employee, but I was useful and smart enough to keep it as well, and had some reasonable progression. For a while I’d been renting rooms after financially over-extending when I lived in my flat, and that job gave me the much needed anchor to my life. Eventually I bought a house with my then girlfriend. That stability then allowed me to think about taking a risk again… But it also established a nice final salary pension plan that will still be useful even 40 years after leaving!

I went contracting

Sometimes, income really matters. I don’t think contracting is for everyone. I hated some aspects of it, and it ruined my relationship at the time because I was away from home so much. But it really helped bring in money, which then really helps you to just establish a buffer of more than a month or two of money. Suddenly I felt like I had an actual surplus and proper savings. I got rid of the rust wreck of a Peugeot and bought a three year old Rover. I started to dress more smartly. I had nearly ten years of this solid and high income and it probably made the biggest difference of all to me.

At the end of my ten years, inflation and low interest rates made my mortgage look tiny, I had asset wealth in the house, shares, and low outgoings. When you’re in that situation, as many middle classes get born into, you can start to take risks. I decided to set up a proper web development business, now called Interconnect.

I could have lost a lot with Interconnect, and we came close to giving up. It didn’t ever give me more income than contracting – not even close. But it does give me another source of stability. And that, dear readers, is worth more than you might think.

I learned about how money and how the stock market works

There’s one book I read early one which just opened my eyes to the world of money. I’ve bought it several times, lent it to people, forgot who I leant it to and lost it! Doesn’t matter, it’s worth it. Its called How The Stock Market Really Works and it goes way beyond stocks, shares, and bonds, but into planning, risks, retirement and so on. In reading it, several times, I established a baseline of understanding that stopped me falling for scams, stopped me making bad investments, and generally helped me ensure I could make best use of the spare money I had.

I no longer pushed my finances hard

Now I understood money better, I knew that, for example, if you have assets of £100k and a debt you can’t pay of £50k, you’re in a really really bad situation. If you have assets of £10k, a debt of £100k and some short term cash flow issues, then you’re in a strong position to start negotiating. Why? Because if you have no assets and a big debt, the bank can’t recoup anything much if they send in the bailiffs. Once their costs are accounted for, they lose everything. So they’re more willing to negotiate. If you have loads of assets, you’re stuffed. That was, in effect, what the bank did to take my grandmother’s home from me when I was younger. They had no motivation to negotiate with me.

So you either max out your finances, Donald Trump style, or you very carefully segregate them. Because I value stability and security above all else, I segregate them.

I learned to think like an accountant

After ICI, I spent a lot of time working in corporate finance departments on their software.

Here’s a thought experiment. You have £10,000. You go out and buy a car for £9,000. How much are you worth? The naïve answer is £1,000. You see yourself as £9,000 worse off. But if your car helps you earn more money by opening up a job you otherwise couldn’t reach where you’ll earn £5,000 a year more, then you have two things happening:

First, your balance remains at £10k, because you have a £9k car and £1k of cash.

Secondly, you have a future benefit over, say, the five years you expect to have the car, of £25k. So over the five year period, assuming the car becomes worthless, you’ll end with £26k on the balance sheet. Or you use that £26k to put into a mortgage which, again, is generally a good move because it’s a limit liability loan secured on property which, in most economies, is a pretty safe bet.

But all accountants will say that cashflow is of utmost importance. You may have a pile of assets, but if you can’t service your responsibilities then you become insolvent – you can’t always easily sell assets without a big loss. So always think about cashflow – it’s best to be gently increasing your cash position as your wealth grows.

I learned to let go of status plays

When I was young I caused myself trouble by buying that sports car. It wasn’t, in itself, a bad buy on the surface – sports cars depreciate more slowly, the insurance on this one was the same as a similar powered Ford Escort, and it didn’t use any more fuel. And it’s not like a 19 year old needs to carry a family. Two seats was fine. Reliability wasn’t great either. But where it went wrong is that my boss therefore believed he paid me too much! My older superiors didn’t like that I had, on the surface of it, a fancier car than they did.

Of course, I was financed to the hilt, and they weren’t. They didn’t know that. They just assumed I had more money than I let on to.

Had I been in a humbler car, they’d have had no idea of my financial status.

It’s better to let people assume you’re a bit skint, and focus on reliability plays in order to establish your career. Took me into my thirties to work that one out.

Same with clothes. Stick to cheap clothes until buying them is easy. If you do what young me did and buy everything on credit at Top Man and Burton’s (yeah I know) then you’re setting yourself up for bad decisions and bad outcomes.

Adaptable accent and open attitudes

I’m actually quite Scouse yet a lot of people I meet and work with down South just think generic, educated Northerner with a light accent. The reality is I just adapt my accent to suit the situation. This means I don’t terrify upper middle class people, whilst I can still sit and have a chippy lunch with garage mechanics. Non-threatening to everyone, basically. I accept that most people know stuff I don’t, that they believe they’re trying their hardest (they may not be trying optimally, or coping badly, but I accept their belief), and generally try to learn from the people I meet.

Meet lots of people from different backgrounds

The more people you meet, the more lives you get to understand, the more mistakes you can avoid and the more opportunities can come up. Local politics can teach you how councils and Westminster works. Bankers can tell you how finance works. Medics can give you really good reasons why you shouldn’t smoke, drink, or eat too much sugar! Bin men can teach you that you can make a good living even if you’re not well educated (or are – there are some very well educated bin men and women out there). Truckers can tell you how their industry works.

Just avoid the cynical and the put upon – there’s little useful information there.

One good thing with the internet today is that there’s so much sharing online that you can virtually meet almost anybody, from African villagers to corporate board members. Just be kind and open and remember that they’re all humans, every one of them.

What about you?

None of the above is unique to me, or in any way makes me special. I just think they’re what helped me. Feel free to comment on what you’ve experienced. Everyone lives different lives and found different ways out of poverty traps. And of course, some people find themselves ground down by a system that can be unfriendly and downright hostile at times which means they can never escape, no matter how hard they work.

In my previous post, I discussed the importance of separating wealth from income, and to stop beating up a chap called Rob Barber who made the mistake of having a high income but not feeling rich. I get exactly where he’s coming from because I’ve been in the same position. In fact, it was more dangerous, because I made the mistake of thinking I was rich before having a sudden epiphany.

In the hazy distant past of my life, I worked at ICI from 1987 to 1997. It was a good ten years, in many ways, because although it started skint I acquired the skills and knowledge to make life a lot better for myself. I didn’t appreciate it as much as I should have done at the time, but in part because being skint at 18 is equivalent to trying to get out a pool of oil. Slippery and error prone.

In that time at ICI, and in the years when I left to become an IT consultant, I worked on payroll software and corporate financial software. When you code something into software, you have to know the subject intimately. Everything I code, I learned about in great detail then explained to a dumb computer. Programming is a really great way to understand things – a computer is like a very patient, dim student with fantastic memory. And when you teach, you learn. You have to.

So I remember when I was around twenty-five some of my older colleagues would always go on about how they hoped for early retirement. This seemed dreadful to me, because I remember my grandmother’s retirement in poverty. But what I didn’t know was how much things had changed.

These colleagues, you see, had a defined benefits pension scheme and ICI was a company on the wane. It needed to reduce headcount each year. One way that a department could reduce headcount was to retire people early, as young as fifty. Today I’m fifty and the idea of retiring and not being poor just isn’t there. I’d be quite hard up. So how could these guys get excited at the idea?

Defined benefit (DB) pensions vs. defined contribution (DC) pensions

All those guys retiring in the nineties onwards were born around 1940 onwards. They started work sometime around the early to mid sixties. And they won life’s lottery big style. They had two key things going for them. 1: the economy of the country was growing fast after the war, so there were lots of opportunities for work, and 2: because of a difficulty in hiring people, firms needed to find ways to attract and keep staff that was cheap at the time and hopefully kept wages down a bit.

At ICI, we were all on what’s known as a “defined benefit pension.” That means that the pension you get is defined according to a set of rules. If I remember rightly, the rule at ICI was quite simple – you got 70% of your final salary. This kind of final salary scheme exists today in only a few legacy situations or with older staff in some firms.

I remember thinking how it was crazy that a 50 year old with thirty years of experience could then look forward to another thirty years on 70% income. Given the reduced costs of retirement (no commute, no need to keep smart work clothes, etc) it was almost like having a full salary. Not only that, many would take a consulting or part time job and be on substantial incomes. They would earn more money in retirement than they would during their working careers!

I smelled a rat! The maths didn’t work out. As I then worked more and more on corporate finance I got to know a lot of accountants and some financial directors. I asked about this problem and they all said one thing: “Those pensions were promised to people by directors who are long gone, and mostly now dead. Totally unaffordable and the company now has to make up the gap… or go bankrupt.”

If you’ve ever wondered why so many of the giant companies of the UK that existed in the sixties are no longer with us, then that’s one key reason. Pensions. At one point, Rolls Royce was putting over a third of its gross profits into pensions. British Airways was once described as a massive pension company with a small airline attached.

Moving on to your situation today – now you have a defined contribution scheme, if you start a pension scheme. It’s generally a good idea to have a pension scheme, especially because the UK government encourages it with generous tax breaks on contributions. Both you and your employer can contribute, within limits.

A defined contribution scheme (DC) is based on the money you put in, and that’s it. In many ways, that makes more sense. But how does saving a portion of your salary get you close the pensions your grandparents or parents got from large employers like ICI, universities, and the public sector? A hint… it doesn’t.

The great wealth shuffle

What’s happened, and it’s absolutely not the fault of the benefactors, rather than of cynical weasels that are long dead, is that wealth has been shuffled to the older generation in a very effective way. Not all older people, sadly, but those who had decent jobs in decent employers and owned their own homes did best, whilst those in more casual employment, rented their homes, and didn’t realise the importance of savings are left with nothing more than a state pension… so they did the worst and can still be in relative poverty. Unfortunately, if you’re not thinking and acting carefully today, your retirement, even if you work in a good employer, could be a lot more like that poor old person’s than you think and a lot less like your grandparents with their motorhome and three bedroom house.

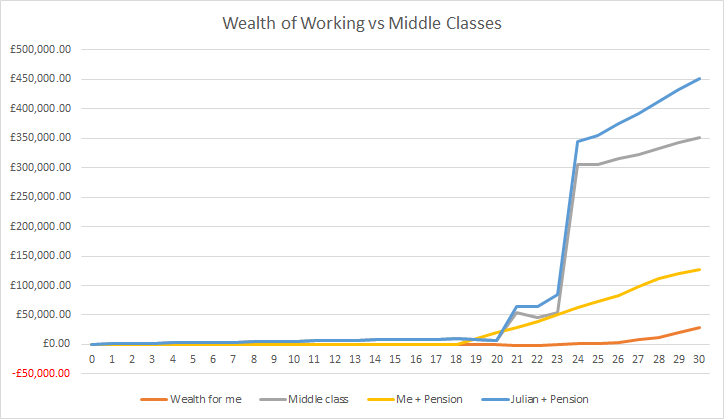

So, I like charts, right? Remember this one from the last article?

That shows my wealth including the value of my property, savings and other bits and bobs like a car up to the age of thirty, with a different line for a middle class person with the same career.

Let’s see how that changes if we take into account the defined benefit pension scheme I had at ICI. I then didn’t contribute to a pension scheme until I was in my forties, mainly because I had other priorities and, well, I knew what I was up to. But for most people that would be terrible advice. Don’t do as I did!

Take a look below:

Now, do you see the change? In fact, for one glorious year in this story I was ahead of the middle class chap called Julian from the previous post! It wasn’t to last, because we’re assuming he worked in the same way I did and had the same sort of career, just a few years later.

Just so you know, I worked out the pension wealth on a simple basis – it was worth, based on my leaving salary, the equivalent of £100k if I tried to buy an annuity, because today, to give the benefits I can still expect from my pension, I would need about a £200k or so fund in order to buy an income equivalent to my defined benefit. I hope that makes some sort of sense. In essence, I count my pension scheme as being a £200k bit of wealth that I don’t think about.

Defined benefits pension schemes made people who started work before the mid-nineties surprisingly wealthy. It’s just not fungible.

What does fungible mean when it comes to assets? It means that the money isn’t readily available. A bicycle is fungible. You sell it for cash, and can sell it quickly. A house isn’t terribly fungible, but still better than a pension scheme because the pension scheme is sort of a bet. It can release some money to spouses, but doesn’t necessarily have to – that depends on that defined benefit.

So my ICI company scheme increased my effective disposable income in those years by more than 100%. I never even realised it at the time, because I only really learned properly about money in my early thirties.

So now you know how that sweet little old lady with the poor education, who worked at a factory, has managed to afford a decent pension with three annual holidays and a mobile home near Carnaerfon.

So this is good, right? We made older people richer!

It is fantastic that older people were made richer. The only slight fly in the ointment is who paid. And why. And why it could be better.

First of all, remember above I pointed out that companies had big shortfalls in their pension funds? Well, if they had to find £5,000 for each year that I worked extra, that had to come from somebody who currently works at the company, and from the dividends. But if all big firms cut dividends, all pension funds (which hold shares in big firms) would have had even bigger shortfalls! And share values would have gone down, making these firms vulnerable to aggressive takeovers.

Reality is, and this is all a layman’s explanation without too much detail, that younger people paid to make older people richer, but without having the same future benefit for themselves. The older generation, realising the problem, and now running companies, took away those benefits wherever possible.

Pension funds also being large shareholders and needing their income, also pressured companies they held shares in to return greater profits! So that meant that younger people’s incomes were pressured in another way!

At least young people have avocados now?

Well yes, they have access to avocados. But not houses – they’ve become more expensive, because with people living longer, and fighting any development that may affect them and their neighbourhood, young people can’t afford houses. A starter home in my home town of Widnes is around £200k. That’s a *lot* of avocados you’re going to need to cut back on to make a dent in the wealth differential. Relatively speaking, my grandmother bought a brand new starter house for £17,000 in 1984. Which is about £55,000 today. Good luck buying anything other than a tiny ruin in Widnes today for that sort of money.

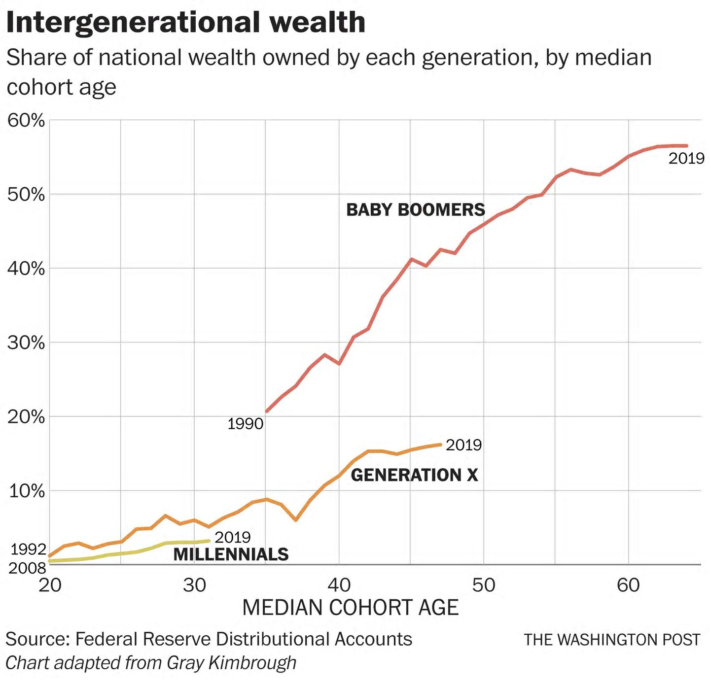

Houses and pensions have led to the following interesting chart:

Now, this chart has its caveats, and I recommend reading the full article here, but let’s face it, with these sorts of gaps, Rob Barber is going to have to earn £85k (a lot less after tax) in order to catch up with a well established boomer. And let’s not discuss how much harder it is if you’re working class and end up supporting the boomers that didn’t do so well on the pensions lottery and had more casual jobs. Life is harder if you started poor.

There’s a bloke who’s been on Question Time who makes £80k a year and claimed he’s not in the top 5%. Which clearly makes him a moron and a subject of derision, right? Sock it to the wealthy! They’re all bastards who need putting in their place!

Well actually, he’s not. A lot of people arguing about him are misunderstanding him. Mostly through their own equivalent ignorance.

Now, I don’t know too much about this guy, but in the way he dresses, talks and where he comes from I’ve noticed a few things.

He and I are super similar, but he got a better start in life than me. He’s even doing well as an IT consultant, like I did. And he likes racing motorbikes. I liked racing a Lotus. Both of us have good lives, relatively.

I don’t feel rich either. I know I’m richer than a lot, but I’m still poorer than a lot too. And now I’m going to explain why someone working class, like Rob Barber or myself from relatively humble backgrounds don’t get to feel (or be) as rich as Julian Middle-Class from Surrey even though our incomes may be substantially higher. Because the system is rigged against us, dear reader, and not against the wealthier middle classes.

Those of you who are working class and shouting at Mr Barber are perpetuating this. I’ll explain this over a few key thingies (it’s an official term for worked out stuff, stick with me), using graphs and stuff. I hope it helps. Today is part one, reaching thirty.

1. The starting point

When I was 11 I went and lived with my granny. Lovely, batty lady, from a well off family, oddly enough, but had fallen on hard times through a bad choice of a first husband, deaths, and poor financial planning. We lived in a caravan. It wasn’t a pleasant experience.

I don’t know much about Rob Barber’s early life, so instead, I’ll just do a chart of my approximate wealth from childhood to the age of 30 (I’m now fifty) and, for comparison, a similar middle class person who also gets into IT and starts consulting at the age of 27.

Now, let’s take a look at this hastily drawn chart.

I’m very very different to that middle class person. But why? Well, for starters, the middle class parents carefully saved £500 a year and put it into an account for their kid. I had no such luck. So by the time Julian Middle-Class was 18, he had nearly £10k saved to help him in university. I didn’t. I didn’t even have a home and my grandmother was clearly getting older and less able to look after me. I decided I should really work as soon as I finished my A-levels.

In theory that should give me an immediate advantage. But my grandmother died just a couple of weeks after I started work. There was really very little for me to inherit except a knackered piano and a broken Reliant Robin. But what I did need to do was find somewhere to live, get transport for work which wasn’t easily commutable. Thankfully I had a decent job and better income than most of my peers. Unfortunately I spent too much on consumables and partied too much. But I was in my late teens with no parental guidance, so bite me. I got into a bit of debt too, which explains the flatlining.

But at 21, Julian got an inheritance when Nana Mabel died. Only £50k in shares. Good job too as during university he’d been burning through those savings he’d acquired from his parents!

So, already, quite the difference. I’m earning and Julian isn’t, yet he’s the rich one in comparison! He’s joined the Socialist Students Revolutionary Union because he thinks he’s poor with his lack of income and the state should help him not eat into his capital. He’ll eventually turn into a Conservative. But he’s young and feels skint, so he’s all about wealth redistribution. He means income redistribution, actually, but doesn’t realise it.

On graduation from his Computer Science degree, he spends a year working in a company in London, and takes some risks because he knows that if he screws up and loses his job, he can go home to his parents. The risks pay off and he gets promoted twice in his first year!

I didn’t. I was super careful. I still cocked up, but I couldn’t afford to lose my job, and as employers in the area were generally struggling, there weren’t many options in my small northern town to choose from. I could have moved, but that felt risky.

At 22, Julian decides to buy a modest house. This flatlines his wealth a bit for a while because furniture is expensive and he needs to buy a bit, but it gets him on the property ladder. The furniture depreciates immediately, but the house starts to appreciate right away.

At age 24, Julian’s wealth suddenly spikes! Why? Because his great grandparents died within months of each other. They were very elderly, but in good health and had dodged care home costs. He and his brother got a share in a £600k house which they sold because they had an inheritance tax bill. Julian suddenly starts feeling more, well, Conservative, having seen so much money gobbled up by taxes.

At 26, finally clear of debt, I finally buy a house, cheaper than Julian’s, but about the same size because he’s near London and I’m in Widnes. So at least there I get to feel a little smug.

At 27, we both become IT consultants. Like Mr Barber.

I have a good income, but a good income also comes with some expectations. At a client’s I got the piss taken out of me for my cheap suit. At another I was mocked for my smoky old Peugeot. I bought some good suits and a Rover 600. Phew! But that meant my wealth still didn’t climb as much as Julian’s. Also, property prices aren’t rising in Widnes like they are in London’s commuter belt. So his wealth continues to outstrip mine!

Keeping the working classes down

I’m going to go off on a tangent now. I became an IT consultant not because I was desperate to do so, but because at my large corporate employer I’d kind of hit a glass ceiling. People I’d trained up had been promoted above me. I wasn’t a stellar programmer or anything, but neither were they. But they had Oxbridge degrees and I didn’t. They were on £30k and I was on £18k. I could have tried harder, but going back to Julian’s situation where he could take risks… I couldn’t. I was scared. So I was timid and overly cautious quite often. I was very anxious when on call that I didn’t screw up the payroll of the 70,000 people who depended on my decision during a call-out.

Technical people are often looked down on. It’s something graduates do for a short while on their career paths into corporate management. It sucks. At 18 I was a better coder than half the computer science graduates I interview today, but I didn’t know it then. So I was constantly scared of being found out. I thought I was blagging it compared to those with qualifications. But by the time I was 27 I was over that. I’d acquired a bit of security and stability by then.

Young Julians are currently shouting at Mr Barber, as well as actually hard up people who dream of £80k incomes! Neither should. The hard up should look to him as an example of a working class lad done good. He’s still working class, but he’s cracked the glass ceiling. Good on him! He just doesn’t understand himself very well. Not yet. Give him time.

Coming next

I’m my next post I’m going to cover hidden and typically non fungible wealth. The wealth I had by the time I was 27 and didn’t even realise it.

Ever noticed that there’s a group of people who don’t vote? Good people, by and large… but they don’t vote. Eventually, I think I worked it out.

Ever noticed that there’s a group of people who don’t vote? Good people, by and large… but they don’t vote.

I noticed this during post-referendum chats with our office cleaners. Almost all of them said they didn’t vote. One said she voted for who her dad told her to vote for. I was a bit taken aback.

“But surely if you don’t vote, your interests won’t get looked after?” I asked.

One looked at me and snorted, “Like that happens! Doesn’t matter who gets in, they’re all the same!”

Sounds like a stereotype.

At the time, I wasn’t politically active. Now I am. The time before June 2016 is simply stated as “before the referendum” around here and with most people I know. As referendums go, it dwarfed all others. The Referendum, it should be. Because at that moment, a lot of things changed.

And, unusually, a lot of people voted. They voted for a change, and they were told it would make the NHS better and leave the country with more money.

I was deeply upset. I kept arguing with the hardcore Leavers, and then, in private, a friend sent me this message:

I’ve read a lot of what you have shared about the referendum, and as I leave voter I now fear I have made the wrong decision. I didn’t envisage the racial attacks that have since occurred, and did not vote out on the basis of immigration. I come across some of these people in work, and you then realise these are just normal and friendly people on the whole. I don’t have a great knowledge of politics and this is dangerous, as we all have the option to vote. I almost never voted, as had no strong bias to either side. I guess I’m trying to say your passion for remain has made me sit back and look at things from other people’s views. I can see you want the best for people. I wish I realised sooner, although it wouldn’t have changed the result.

Thing is, a lot of people realising sooner would have changed the result.

But people like me… we voted. But we didn’t try, did we? I know I didn’t protest, or man a stand in the streets. Had it too easy, you see. I thought others were doing it all anyway. Different people.

Let’s go back to our cleaner. Why didn’t she vote? Because she didn’t feel like she made a difference. Like she was going to get the shitty, difficult end of the stick either way. Not only that, but politics felt unreachable to her.

The Referendum got more people engaged, largely because a simple promise was made. £350m more for the NHS.

And people, even in post-Brexit Halton are still worried about the NHS. Here’s a local survey I did about concerns – sample size not massive at 67, but it’s enough to be a reasonable representation for the Halton area.

NHS is important. People worry about it. Because ultimately, we all get some sort of health problem at some point in our lives. Or our kids do. And we hear the stories of bankruptcies faced by US citizens due to their harsh private healthcare system.

Then Brexit and UK stability came in highly. And education. These are people’s primary concerns. I was actually surprised how few were worried about the benefits system, but then unlike the popular image of the North, most people aren’t substantially dependent on benefits. At least not in Widnes and Runcorn. So it’s not their biggest priority.

But let’s get back to our cleaner. Why doesn’t she* vote?

Unfortunately she couldn’t articulate it.

So I decided to remember what it was like when I was young, skint and facing homelessness. At no point did it occur to me to contact a councillor or my MP to see what could be done. They were distant people. Different people. Like teachers. I remember the shock and surprise when I learned that teachers had to go to the toilet! Yes really – they too need a wee sometimes. Amazeballs.

When you’re relatively naive, you don’t see the world all that clearly. Business-people are different. Asian people are different. People from the next town along… are different. It doesn’t matter. If you don’t know people, they’re different.

And most people don’t really know their local political parties. In the thirty years during which I’ve been able to vote, I’ve only heard from politicians during elections. I have never ever spoken to one on the doorstep. Except for one short period when I lived in Garston and my MP was David Alton. Now, David Alton has some peculiar views that I disagree with, but he’s a Liberal Democrat, now a Lord, and his councillors would drop in these weird Focus newsletters to the house. And I’d read them! I learned about what was going on in the area. They even had contact details so I could get in touch! They reached out… to me! Weird. But I realised, all politicians should try to do this. Push out their messages.

Then I moved back to Widnes.

And never, ever heard from a politician. Except during elections.

Sure, sometimes they’d say something in the local papers. But nothing relevant to me. Nothing that would fix my problem of living in a shitty shared house. Nothing that would make it easier for me to get a decent home. My parents had been able to get a council house, but it was denied to me. And I couldn’t save enough for a deposit on a house. It didn’t help that I wasn’t great with money either (credit card advertising has a lot to answer for!). But just being a young man, trying to run a car to get to work, renting a room, feeding myself, clothing myself and so on was sometimes tough. And nothing I ever saw from a politician made much impact on me.

Then I got older. And richer. Slowly but surely I made more money. I became a freelancer and discovered a piece of legislation might affect me – IR35. It wasn’t a massive issue, but it affected me. When politics affects you, you get to know stuff.

But working people are looked after by Labour, right?

I used to think that. Many people I knew voted Labour. Always voted Labour. Unquestioningly. I didn’t get it until I learned more about how unions work. Then I realised that unions and Labour are tied at the hip. Which is fine. The Labour Movement was what Labour was about, and it was massively important to the working man. Did a brilliant job.

Sadly, some unions got a bit giddy on power and decided to have battles to get more power. Which is a shame. They’d succeeded at getting working wages and privileges to a good point. They couldn’t see that some of those privileges were unaffordable in the long term. They simply had to keep them. At all cost.

That led to an interesting thing happening. Large organisations such as public sector, NHS and corporates started to outsource more and more functions. Our cleaners are employed by a company employed by our landlords. In many ways that can work. But truth is, that a cleaner at ICI or any other old large corporate like BA would have been exposed to unions, but our cleaners today are not. And even they were, many work for small companies disinterested in trade unions and employing fewer than 21 people. Others may not wish to join trade unions because they don’t like that they fund a political party.

So they’re not represented, really, by Labour. Labour mostly cares about people in trade unions and people who vote for them. People in unions are, for the most part, not the poorest part of society. In fact, I don’t think I know anyone in a union who earns less than about £30k a year once they’ve got five years experience in. That’s one reason why Labour are surprisingly reticent about taxing people in the OK to Quite Well Off groupings.

Nicked from the IFS website.

You could ask why the Lib Dems aren’t harder on the top 2%, but having worked with a lot of that range of people I can tell you that tax on income starts becoming optional at that level. If tax is too high they either put it into various perfectly legal vehicles (pensions and ISAs work well up to a limit) or they start looking keenly at moving cash offshore if possible. And taxing people too much can feel very unfair to those people. Get a £30k bonus and see £20k go to the government. They may not be right to feel like that, but that’s not the point. They feel unfairly treated and so get motivated to look for alternatives. As the IFS study reveals, the Lib Dems would almost certainly raise a lot more money with their tax changes than Labour would.

Labour is the party of the middle classes.

It’s true. Student fees position? Well, the current regime of student fee repayments introduced by the coalition means your repayments are lower if you earn under £35k than under the earlier top up fees system introduced by Labour.

Pensions position? Most of the people affected are people with good pension incomes. They are not poor people. Poor pensioners are considered in a secondary way, because they do at least vote. But most of the policies continue to leave wealthy pensioners paying far less in tax than young people on equivalent incomes.

The unions? Most union members earn good money. According to a study by the Department for Business, Innovation and Skills, trade union members were paid an average of £14.45-per-hour, 5p more than in 2012 (£28k/yr, equivalent to over £30k/yr today) – source

So who does represent the best interests of our cleaners?

I say the Liberal Democrats. A party I finally got involved with in 2016, after The Referendum. You’ve seen the chart above, and in the early years of coalition, before the Conservatives neutered them, they did a great job of taking low earners out of the tax system entirely. The UK’s Gini Coefficient improved for once!

For more information, see https://www.equalitytrust.org.uk/how-has-inequality-changed

But here’s the problem for the Liberal Democrats. Nobody really knows this. But our doorstep action, whilst being great on a local level, needs to talk about the bigger issues. Potholes and poorly kept parks are important, but these things rarely keep the bulk of people awake worrying. But the NHS does worry people. Brexit does worry people. Not being able to feed the kids does worry people. These issues need addressing. Loudly and proudly.

If you’re campaigning in the 2018 local elections, it’s important to share a little bit about what the Lib Dems mean for everybody. Not just campaign in the middle class areas and get squeezed, but in the poorer working class areas where we can make a big difference. Our policies are better for them. They just don’t know it. Not to tell them this is a disservice to them and to the Liberal Democrats. The working poor need us to help them. And if we reach out to them, maybe they’ll reach out to us. And our cleaners and their friends – they’re essential people, and once they get going they are awesome!